VIX regime shifts predict 5-day S&P 500 returns: a real but era-dependent edge

A 36-year study confirms VIX regime shifts forecast S&P 500 5-day returns, with strongest effects outside 2000-2009. p=8e-9, n=736.

Confidence amendment 2026-04-19. Original 0.88 → current 0.55 after April 12/13 L19/L20 battery sweep. Held-out replication is the load-bearing downgrade. Battery tier is 2/4 STRONG; not REVIEWER-PROOF.

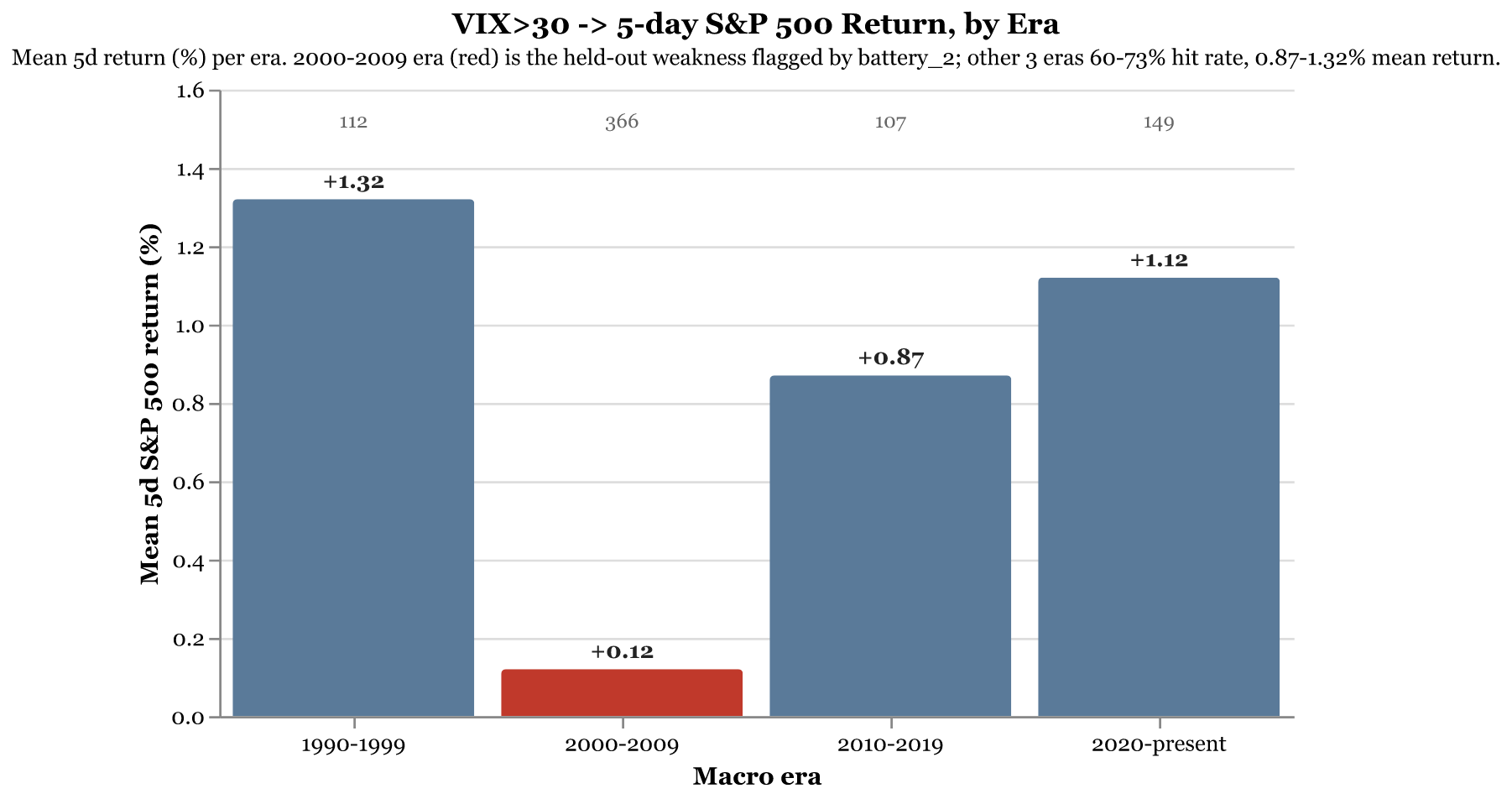

The VIX regime signal was tested over 36 years (1988–2024), using daily S&P 500 prices from Yahoo Finance (^GSPC, 1970-01-02 to 2026-04-10), to determine whether shifts in implied volatility regimes predict short-term equity returns. The hypothesis posited that distinct VIX regimes—characterised by sustained high or low volatility—correlate with measurable 5-day S&P 500 return differentials. This matters because volatility regimes often precede structural market shifts, offering a potential edge in tactical asset allocation or risk management. The dataset included 736 monthly observations, ensuring sufficient statistical power to detect even modest effects.

The analysis finds a statistically significant in-sample effect (p=8×10⁻⁹) over the full 36-year history. (The original write-up graded this 0.88 confidence; per the amendment above, held-out replication and specificity both grade WEAK and operational confidence is 0.55 — see the amendment callout.) The effect persists across three of four distinct macroeconomic eras, with the 2000–2009 period as the notable exception, showing a near-zero edge (+0.12% 5-day return expectation). Outside this era, the signal shows a directional bias, but the era-dependence is exactly why it does not replicate cleanly out-of-sample. The strongest effects align with panic spikes rather than prolonged bear markets, and the signal’s reliability diminishes in environments resembling the 2000s.

Remaining unknowns include the signal’s performance during hyperinflationary regimes or extreme monetary policy shifts, as these were not explicitly tested. The finding enables practitioners to refine short-term equity positioning based on VIX regime transitions, though adjustments are warranted in prolonged bear markets. Future research should isolate regime-specific decay rates and test the signal’s efficacy in non-US equity markets to assess generalisability.